Reasons to be Cheerful, Part 2

Exploring the often grim narrative surrounding UK public finances, offering a fresh perspective on the country’s indebtedness and how government spending, particularly in response to the COVID pandemic and energy crises, has shaped the fiscal landscape.

Neil Woodford

W4.0

Reasons to be Cheerful, Part 2

Neil Woodford

W4.0

Exploring the often grim narrative surrounding UK public finances, offering a fresh perspective on the country’s indebtedness and how government spending, particularly in response to the COVID pandemic and energy crises, has shaped the fiscal landscape.

In Part 1 of 'Reasons to Be Cheerful,' we explored positive economic indicators that challenge the prevailing gloom surrounding the UK economy. Continuing this theme, Part 2 shifts our focus to an area often met with pessimism: public finances.

Most opinions are not especially upbeat and arguably, rightly so. But, as always, the debate about the UK’s overall indebtedness is a little lopsided, so I will try to present a more balanced view here. For the sake of clarity, public finance is the term used to cover income, spending and debt within the public sector.

Commentary on the public finances is generally downbeat. For example, this is from a newspaper article from July last year.

This from an organisation (the OBR) whose near-term forecasting record leaves much to be desired (a subject I will return to in a future blog). Nevertheless, you get the picture.

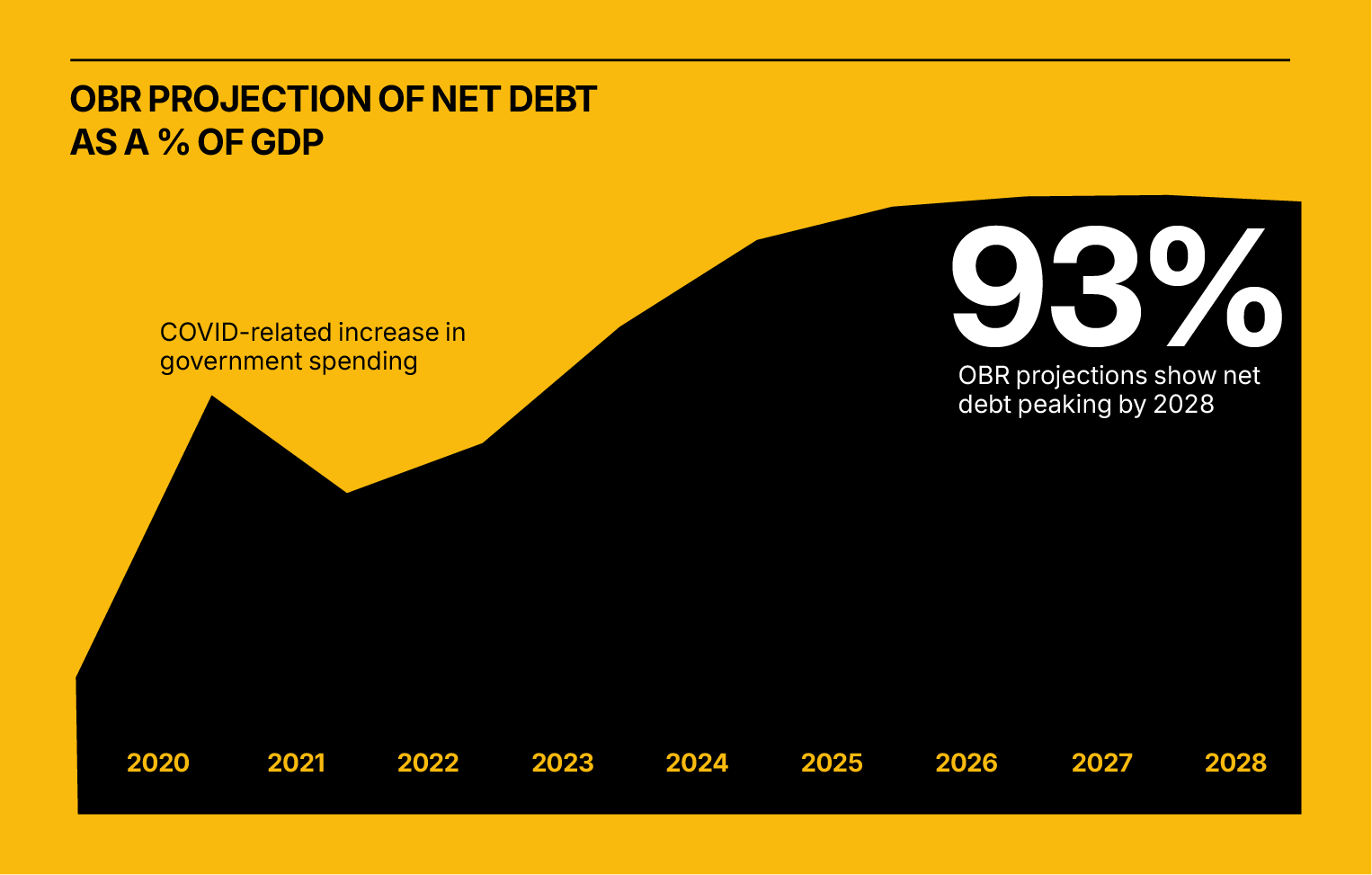

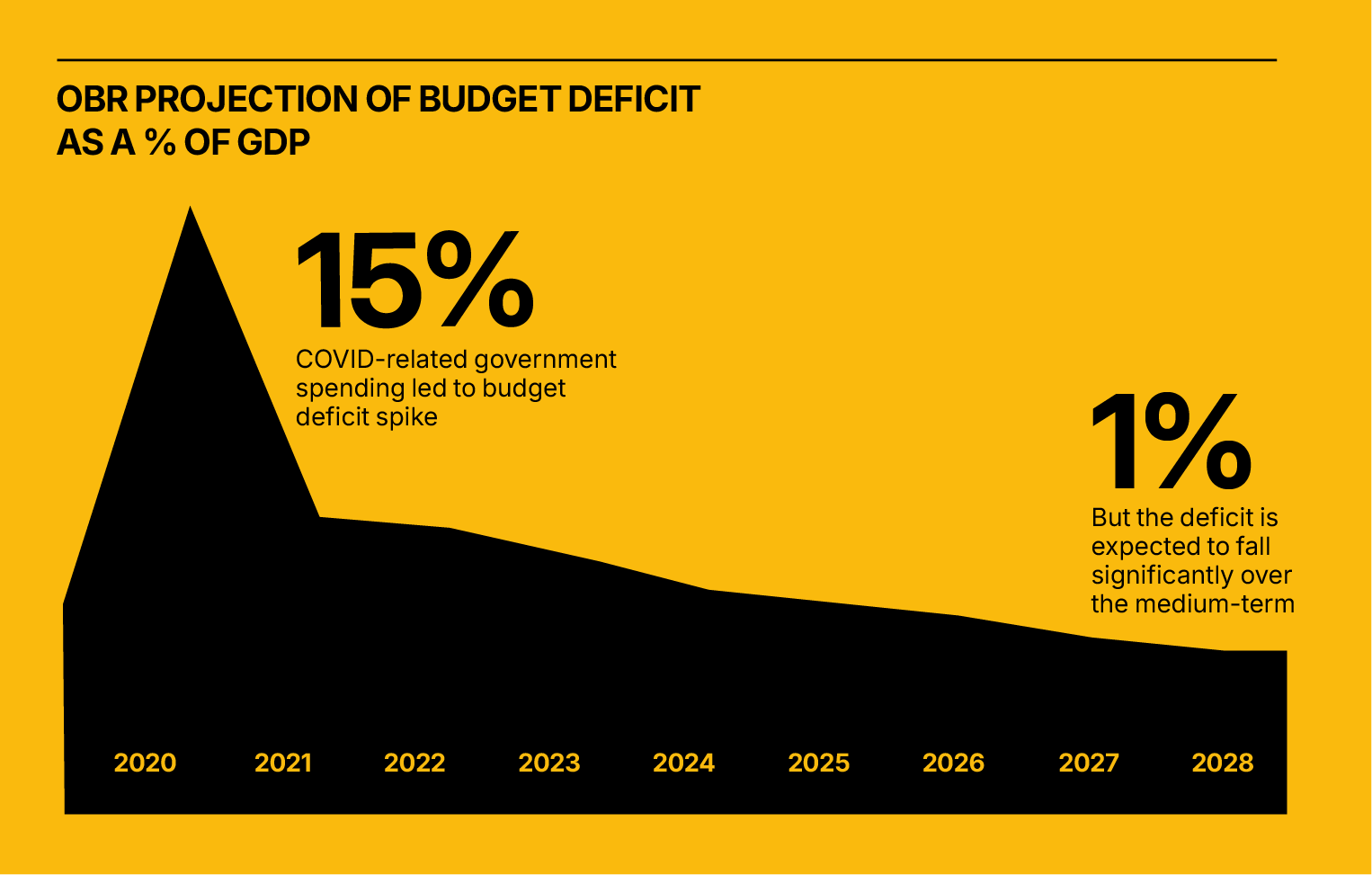

As is often the case, a few charts are helpful to set the scene.

Clearly, debt to GDP has increased significantly in recent years, but this is projected to stabilise and begin to fall in the medium term. This increase is in large part the product of the very significant measures the government decided to introduce during the COVID pandemic and the assistance with energy bills that followed the outbreak of war in Ukraine. As you can see from this next chart, both events and the policy response the government chose resulted in a significant spike in spending which is now normalising.

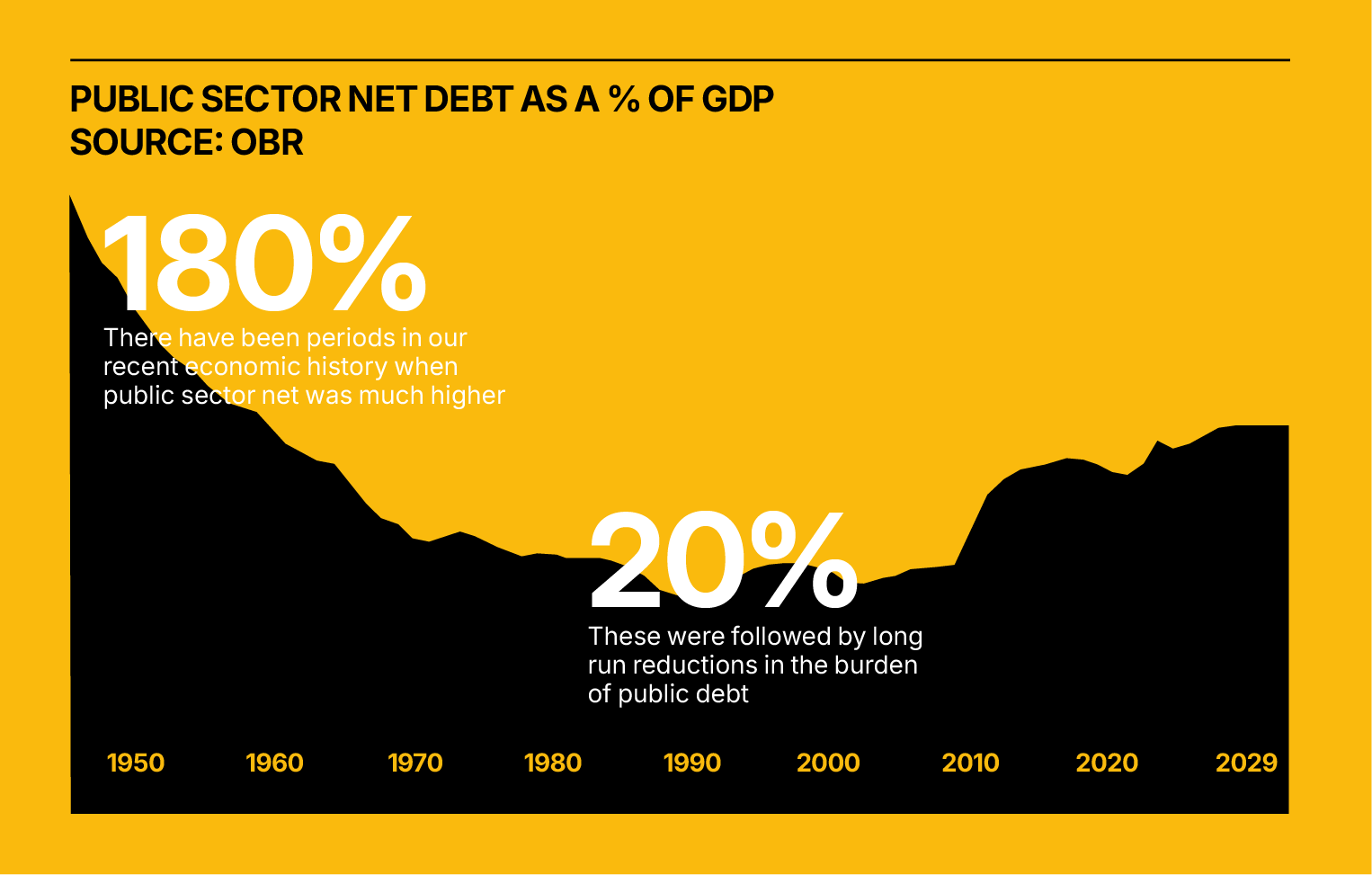

And finally, this chart puts the current level of government indebtedness in an historical context.

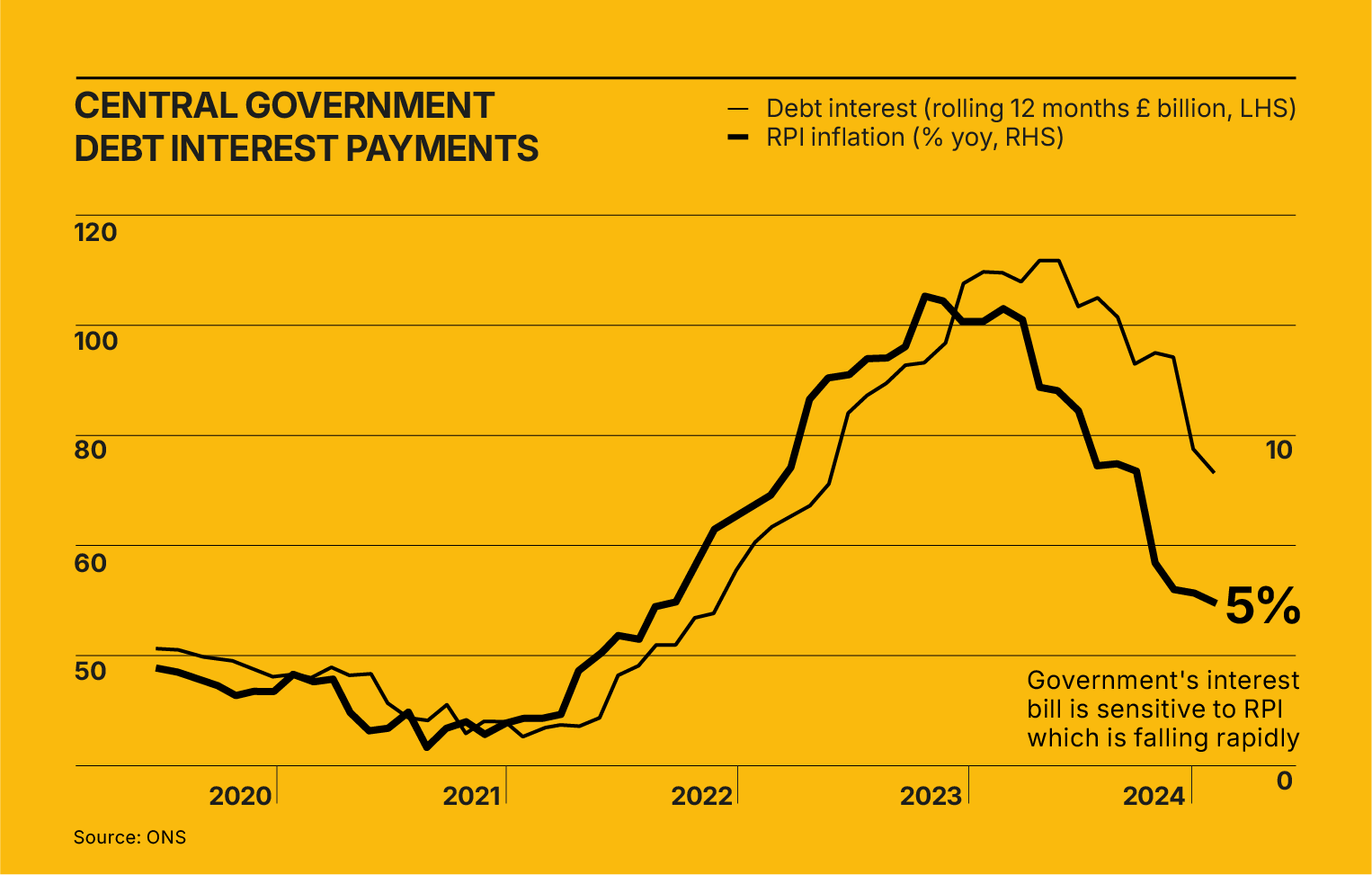

Clearly, government debt is at uncomfortable levels, but this is not, in my opinion, the product of "fiscal incontinence", an accusation that could be levelled at some of our peer economies. This recent growth in spending is clearly the product of an extraordinary series of events that required significant intervention from the government to ensure that the broader economy was insulated from these events’ worst effects. But is it right to say, “Fast-rising borrowing costs are putting UK public finances at great risk?" I think the following chart is quite revealing on this topic.

As the stock of government debt grows, absent prolonged deflation, so will debt interest payments. In addition, because in the UK index-linked debt issuance has been so significant, largely in response to the demand for inflation-linked assets from defined benefit pension funds, the interest rate bill is quite closely linked to changes in inflation. In 2021-22, index-linked interest payments were £35bn but nearly doubled in the next financial year to £67bn as inflation increased significantly. Of course, this is what the OBR was worrying about last July. However, as inflation has fallen as rapidly as it rose, these inflation-linked coupons are also now falling. In fact, the OBR underestimated this decline by about £10bn for the financial year 23/24 in last November’s Autumn Statement. In total, index-linked coupons will be down over £35bn in 23/24 compared with the previous financial year.

Judgements about whether the UK's public finances are stretched or not is moot, but I would argue that in any balanced assessment the exceptional circumstances of the last four years has to be taken into account.

However, this is only half the story. In my opinion, any debate about an economy’s debt burden should also include some perspective on what is happening in the private sector, and, in the UK, this is often completely overlooked. In Part 3 of 'Reasons to Be Cheerful,' this is where we will turn our attention, examining what that means for the overall economic picture of the UK.

Related reading

Reasons to be Cheerful, Part 1

Contrary to popular belief, the UK economy has performed well against its peers over the last 15 years, and the ingredients are in place for it to continue to perform well. In this first post, we dispel the myth that the UK is and will continue to be a laggard in the G7.

Read more

Reasons to be Cheerful, Part 3

Part 3 of 'Reasons to Be Cheerful' challenges the notion of 'falling living standards' in the UK, examining the realities of wages, housing, and employment. This final instalment offers a robust argument that despite recent hardships, the UK is poised for a promising period of growth, refuting the pervasive economic pessimism with hard evidence and a dose of optimism.

Read moreStart investing with transparency

Access our full research, strategy insights, and real-time portfolio visibility.