Punch and Judy Show

The OBR’s “productivity crisis” is being used to justify tax rises on the basis of numbers that are little more than guesswork, while old-fashioned monetary indicators are quietly signalling that something much more positive is happening in the UK economy.

Neil Woodford

W4.0

Punch and Judy Show

Neil Woodford

W4.0

The OBR’s “productivity crisis” is being used to justify tax rises on the basis of numbers that are little more than guesswork, while old-fashioned monetary indicators are quietly signalling that something much more positive is happening in the UK economy.

Once again, I have been stung into action by the relentless drivel emanating from the financial media and politicians. This prolonged pre-budget period has provided fertile ground for those with an opinion to voice it loudly and repeatedly. Unfortunately, the facts, once again, appear not to be relevant to this discourse and certainly play no part in the weekly Punch and Judy show at PMQs in the House of Commons. In general, the government comes under pressure for its tax-and-spend policies, whilst Kier Starmer accuses the opposition of causing the productivity problems that increasingly appear to be at the centre of the debate about what the OBR will say in a few weeks, and how the Chancellor will respond to those forecasts.

To describe this situation as ridiculous is to flatter it. The economy waits with bated breath whilst the ONS, OBR, Treasury, Chancellor mumble**** decides what will happen to the taxes we will pay, apparently based on their collective finger-in-the-air judgement of UK productivity over the next five years.

Bear in mind that productivity is something the ONS has been incapable of measuring accurately in the past, and which, ironically, was upgraded significantly following the upward revisions to GDP a few weeks ago. Remember as well that the ONS has itself cast considerable doubt on the accuracy of its employment data (the Labour Force Survey), which it in effect believes is overstating the number of people in work (this is the denominator in the productivity calculation). Finally, also remember that the OBR has itself described productivity forecasts as uneducated educated guesses (to paraphrase).

It beggars belief that the Chancellor will apparently have to base her tax decisions on what are effectively guesses for both baseline and downgraded forecast productivity, just after it’s just been upgraded following recent upward revisions to nominal GDP, and ahead of what is widely accepted as a productivity industrial revolution as AI is rolled out across every corner of the economy. The application of a modicum of common sense might dictate that five-year forecasts of future productivity should be increased, not downgraded right now, to reflect the impact of that industrial revolution, but unfortunately, that sort of pragmatism appears to be in very short supply in the corridors of power.

One might have thought, given the inherent flakiness of productivity measurement, that instead of treating it as an input, the collective wit of the OBR would be focused on trying to assess what growth the UK economy might deliver over the medium term based on a more straightforward judgements of, for example, what households will be spending in the future. That, of course, will be a function of their collective decisions based on incomes (more easily forecastable), savings (a known) and borrowings (a known) and how these evolve over time in response to lower interest rates. (see below) Through a process like this that also looks at government spending (pretty predictable) and investment spending (which is growing and starts from a £42bn higher base following recent ONS revisions), it should be possible to get a pretty well-informed view on what will happen to growth (output) over the next few years. Based on trends in employment and hours worked (NOT the Labour Force Survey, or LFS), it should then be possible to calculate changes in productivity as an output. That’s what I would do. It’s a lot more straightforward and, in my view, a more reliable way to anticipate the future. Unfortunately, I suspect the OBR will default to its more arcane approach, which has historically been long on complexity and, frankly, poor on accuracy in relation to outcomes.

Quite why the inherent volatility and historical unreliability of productivity data have not led to a more circumspect attitude toward its use as a predictive tool is bewildering. Just by way of example, take recent history. Productivity fell in the UK in 2023 and 2024, according to the ONS, yet economic growth was positive in both years and indeed accelerated during this period as the economy recovered from the energy price, inflation, and interest rate shock that followed the Russian invasion of Ukraine in February 2022. In 2024, according to the ONS, output grew by 1.1%, but total hours worked increased by 2%. Anyone who’s worked in a business knows that this isn’t how they work. Successful businesses – namely the ones that survive – don’t use more labour to get less output. (I wrote a blog on this subject earlier in the year that focused on UK manufacturing, which highlights the implausibility of the ONS’s productivity data in this highly competitive industrial sector.)

For anyone that doubts my perspective or believes that this data must be accurate, I would challenge them to have a go at calculating the output of the business that employs them – that is the total amount of the goods and services their business produces over a given period. And just by way of an example, I would welcome suggestions on how to calculate the output of a school during a holiday, or even during term time, or a fire station that has never extinguished a fire, or for that matter, the entirety of Whitehall? What might be the output of the armed forces or of a law firm or an insurance company? By the way, revenue is a poor proxy for output because a business or indeed a government department or the NHS can increase its revenue through actions that do not reflect an increase in its core production of goods and services simply by raising prices. It’s when you start to encounter this level of complexity and guesswork that you can imagine the challenges the ONS confronts calculating output for the entire economy based on survey data where response rates have been falling consistently in recent years.

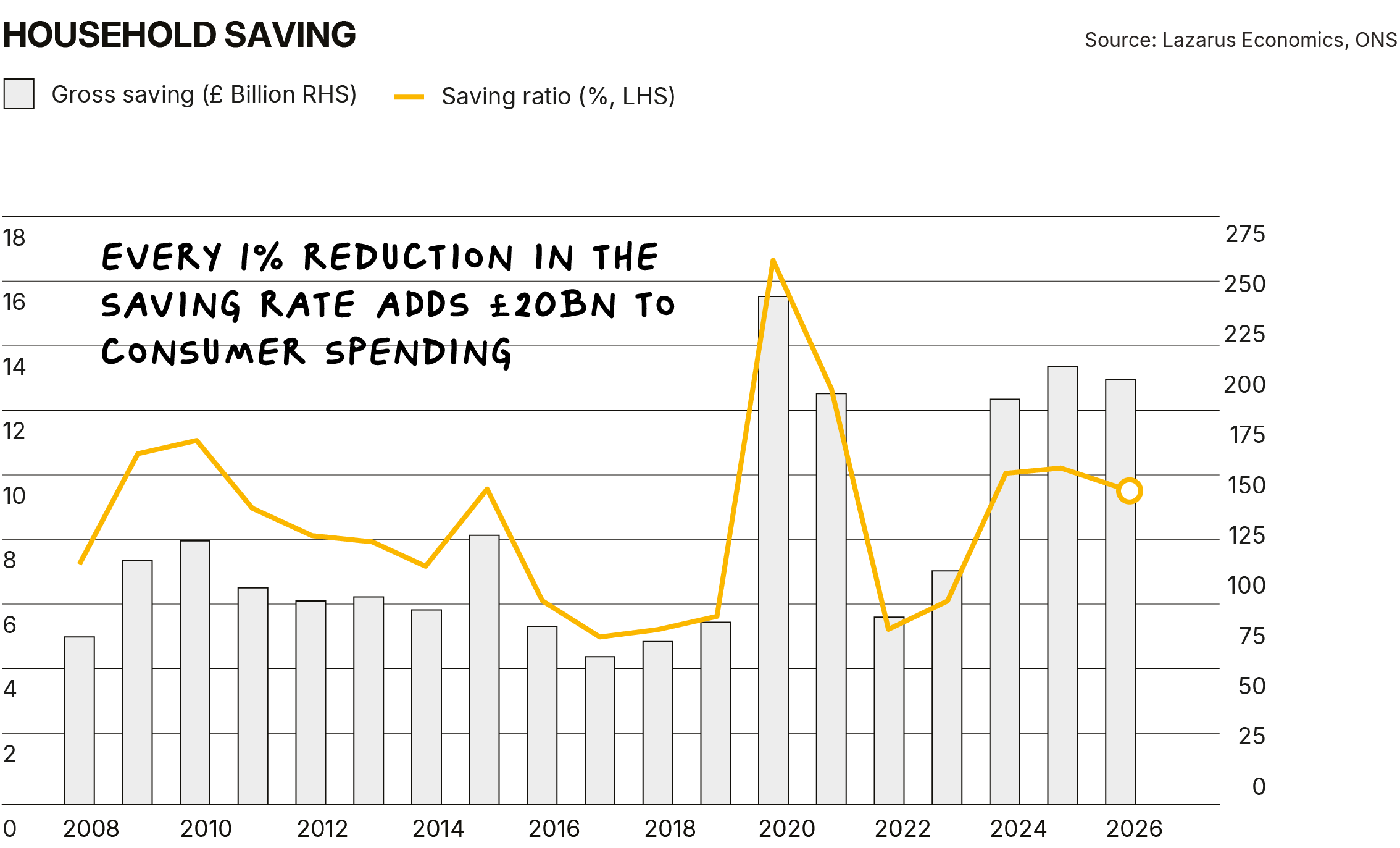

Quite what will happen next week is not yet clear and is unlikely to be so until the Chancellor has sat down on the 26th November after giving her budget speech. I still believe that she should resist the pressure to succumb to speculation masquerading as fact in the OBR forecasts for the UK economy over the next five years. As for what this means for mythical fiscal black holes and what will be done to fill them, my guess remains that there will be tax increases but nowhere near the scale of those envisaged by the media. And finally, for those worried about how tax increases might impact the economy, bear in mind that every 1% reduction in the saving rate from its currently very elevated level of just over 10%, would add about £20bn to consumer spending.

Having dwelt on this rather technical and possibly boring subject, (about which you may have gathered I am somewhat exercised) I thought I should finish on a more positive note. In recent months there has been increasing evidence of better momentum in the economy which has seemingly gone unnoticed in the media and received virtually no attention from economic commentators. Possibly this is because the indicators of this improving economy are somewhat old-fashioned monetary indicators which neo-Keynesian economists (like those at the Bank of England) tend to ignore or dismiss.

Here is a series of easily understood charts that I think paint a clear picture of the economy's momentum.

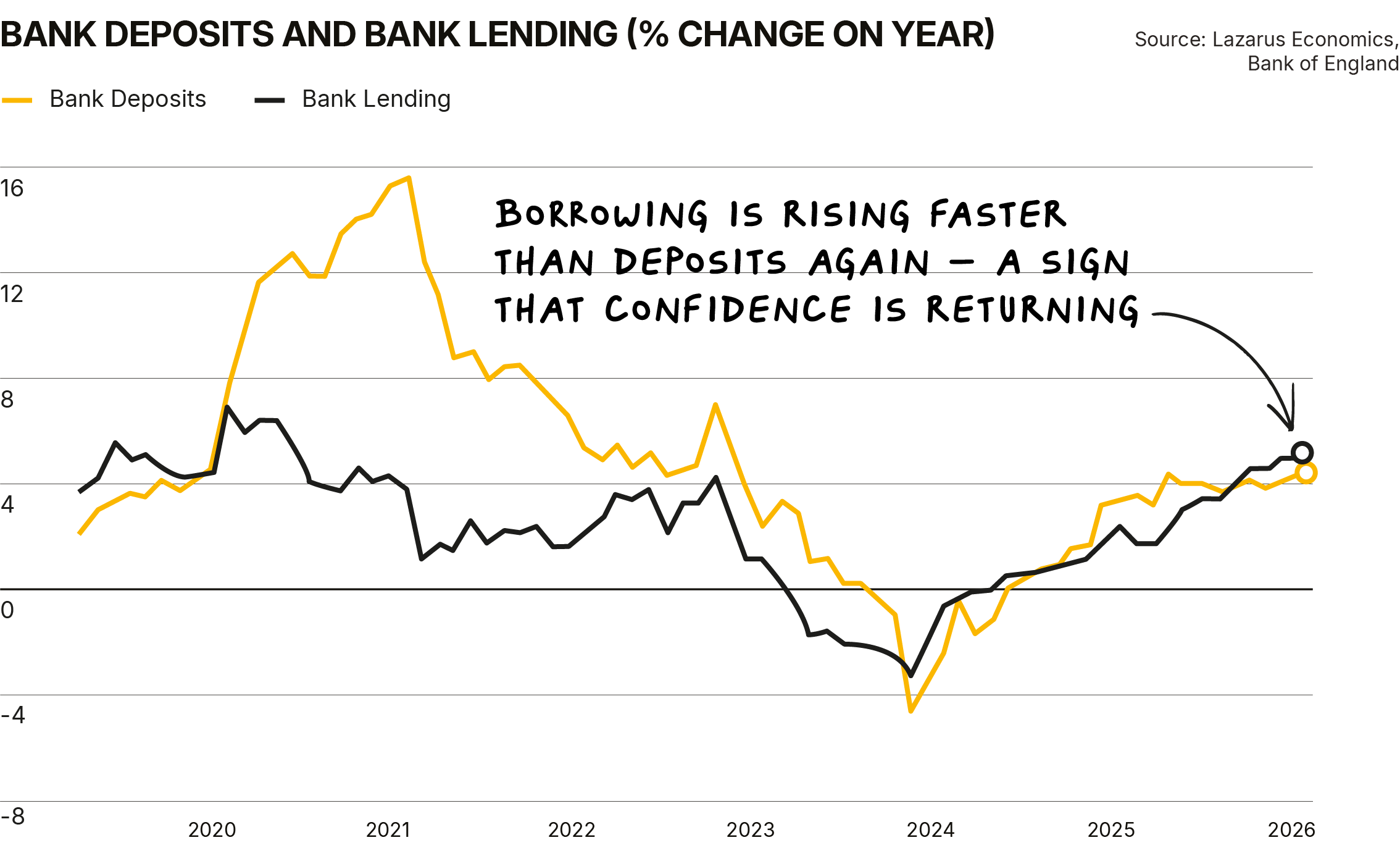

The first looks at loan growth, which, after being negative in 2022 and 2023, is now growing quite strongly in the context of the last five years and is now outstripping deposit growth.

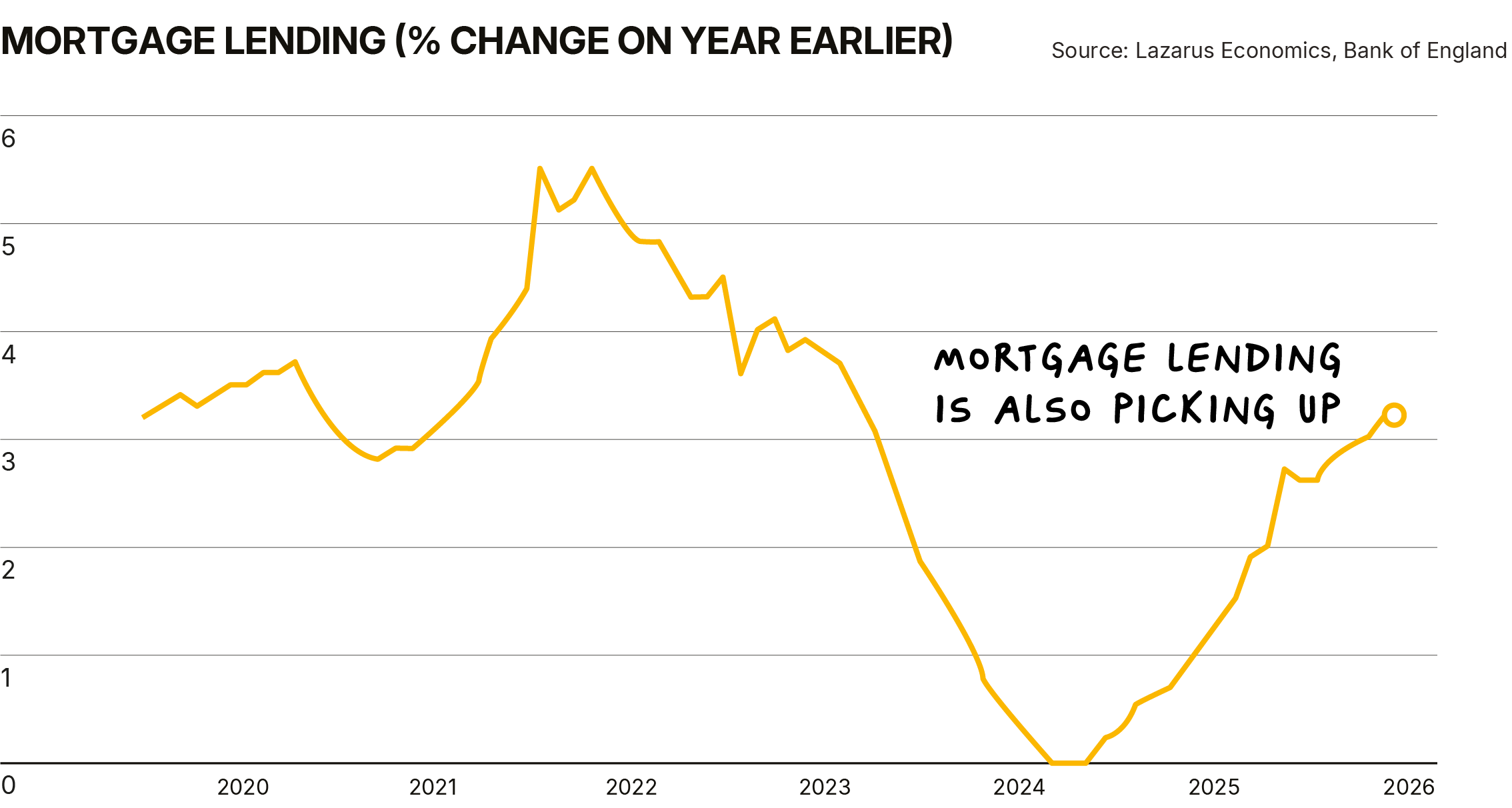

This is reflected in a pickup in mortgage lending and, more recently, stronger growth in consumer credit, which is now growing at over 7%.

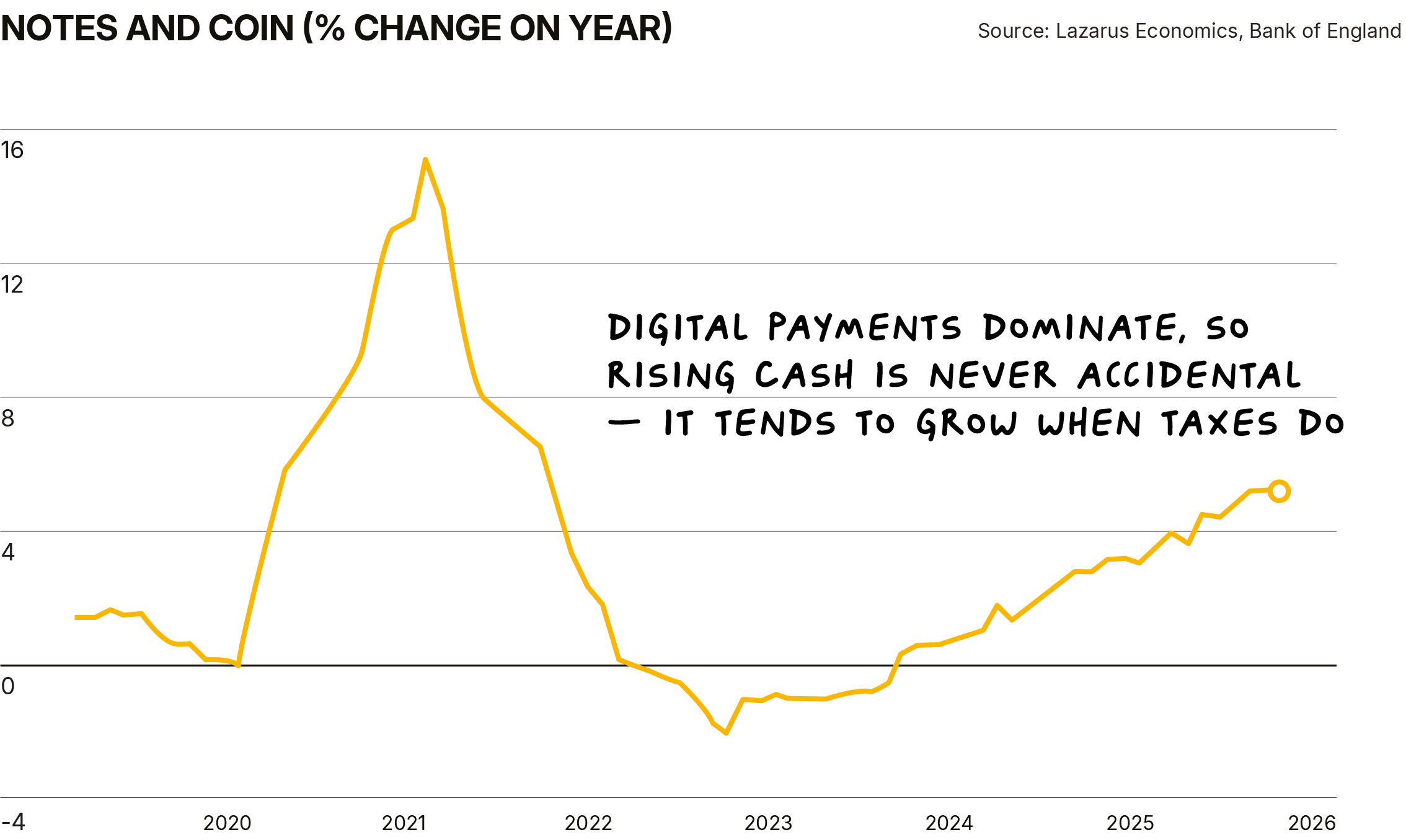

Also of interest is the noticeable growth in notes and coin (narrow money) which may reflect a growing black economy as people seek to avoid high taxation.

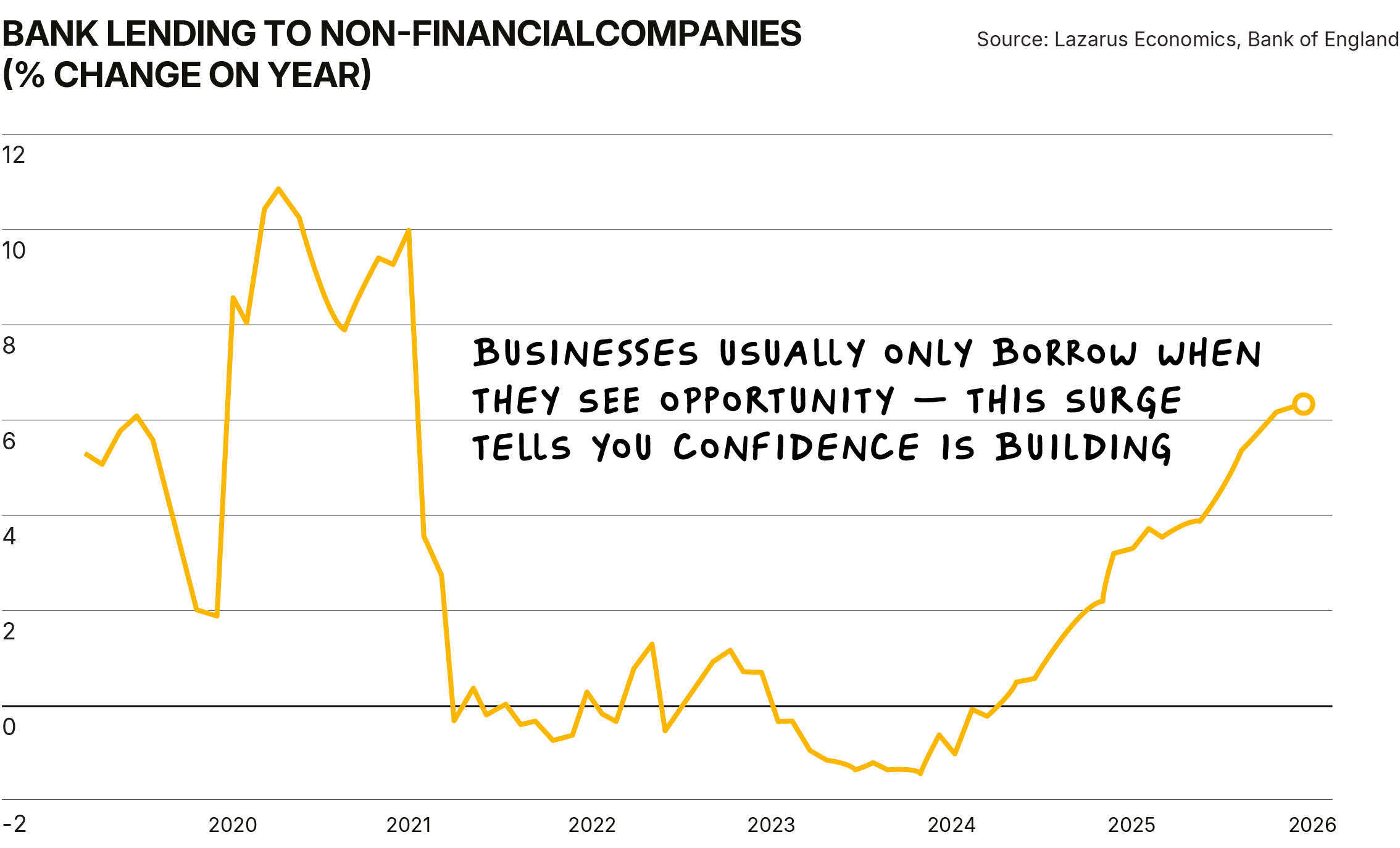

Perhaps most dramatic of all is the very dramatic change in bank lending to non-financial companies. It may be obvious, but it’s worth noting that businesses don’t increase borrowing when they lack confidence in the economy's outlook.

What’s clear to me is that something is stirring in the UK economy right now, and I expect this momentum to build in the months ahead. We will get a cut in interest rates next month and more next year. These cuts will be pivotal in driving greater confidence in the economy, stronger loan growth, more spending, less saving, and ultimately higher growth.

Frankly, my 2% growth expectation for next year is beginning to feel too low. Anyone want a wager?

Related reading

The UAE just walked out on OPEC. The real question is what Saudi Arabia does next.

The UAE's departure from OPEC isn't really about prices — it's about whether the cartel's whole operating model survives. The bigger question is what Saudi Arabia does next.

Read more

The retail data backs us up — the MPC should be cutting

The sharpest UK retail sales decline in over 40 years has just confirmed what Neil warned about on the podcast: the Bank of England's inflation fears were wrong, and the MPC should be cutting.

Read more

The Weapon That Wins Wars?

Why the blockade — not the bombs — is likely to end the Iran war, and why the IMF has mispriced the outcome.

Read moreStart investing with transparency

Access our full research, strategy insights, and real-time portfolio visibility.