Loose lips sink ships

The supposed £51bn “black hole” in the UK’s finances is nothing more than a product of NIESR’s excessively gloomy growth forecasts. The danger lies not in the numbers, but in the media narrative that risks becoming self-fulfilling.

Neil Woodford

W4.0

Loose lips sink ships

Neil Woodford

W4.0

The supposed £51bn “black hole” in the UK’s finances is nothing more than a product of NIESR’s excessively gloomy growth forecasts. The danger lies not in the numbers, but in the media narrative that risks becoming self-fulfilling.

There are times when the UK media’s economic commentary is constructive, sometimes even insightful, but of late, a mind virus appears to have infected almost all commentators on the subject of the outlook for the UK economy. This mind virus was invented in the NIESR’s August UK economic outlook and has infected pretty much every media outlet I can see since, so much so that its central claim that the Chancellor needs to raise taxes in the Autumn budget by up to £51bn has become an established fact. Now the debate has moved on to what taxes will likely be increased and by how much.

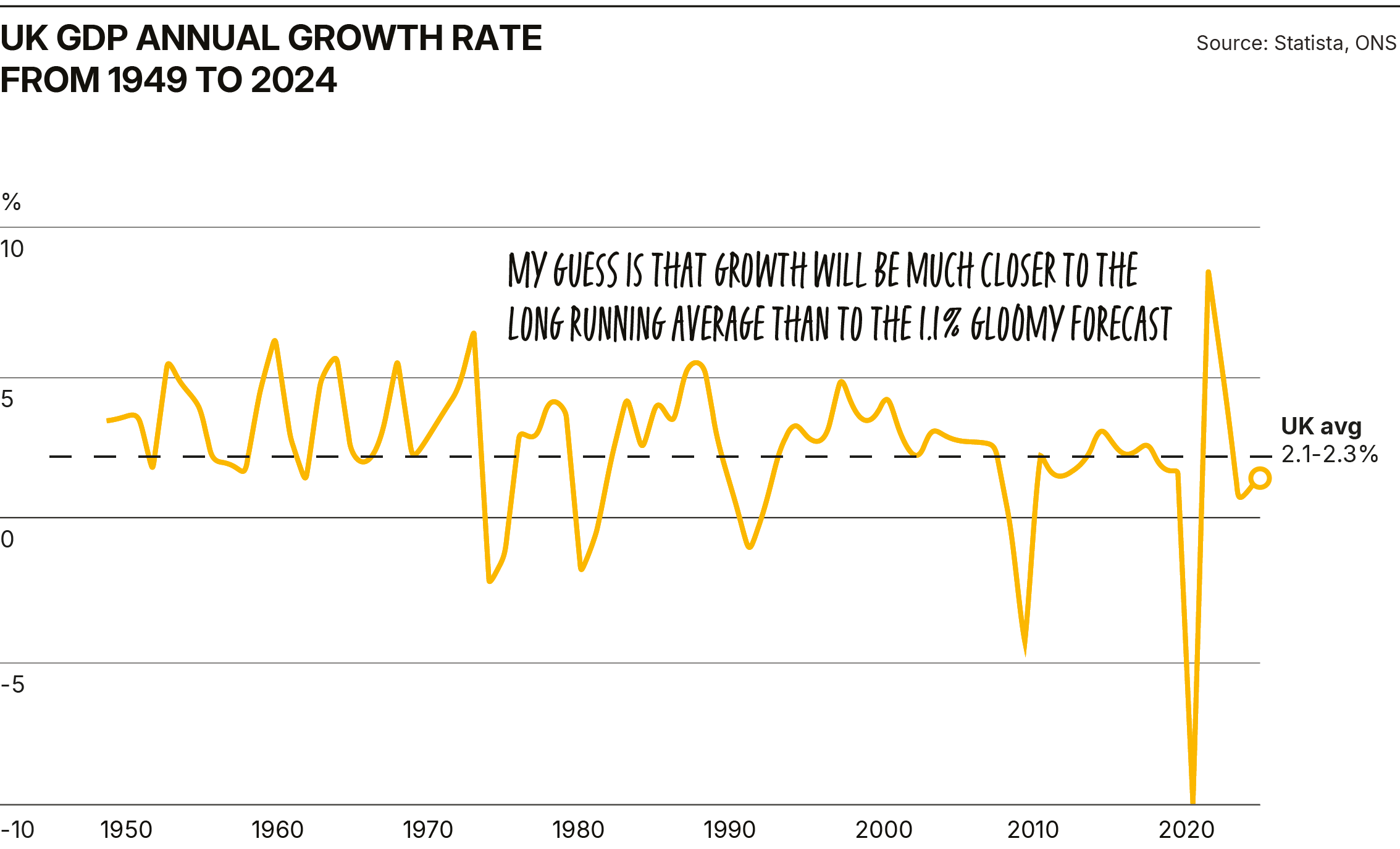

It is this media narrative rather than the facts that is, unfortunately, in danger of creating the very outcome that they have been writing about. The truth, albeit nowhere near as lurid, is that there is no black hole in the nation’s finances, borrowing is exactly on target with the OBR’s spring forecast (in the first four months of 2025/26) and if the economy grows somewhere close to its average rate over the five years to the end of the decade, the current budget (before investment spending) moves into surplus in 2027/28 and remains in surplus thereafter. According to the OBR’s current projections, the overall budget deficit falls to 2% of GDP by the end of the period to 2029/30. So, why the hysterical talk of a black hole?

NIESR’s conclusion that there is a £51bn hole is entirely the product of its very gloomy growth forecast for the UK economy over the five-year period to 2029/30. When I first looked at this story, I went straight to the growth assumptions. They are bleak. In fact, very bleak. NIESR is forecasting growth of 1.3% this year (which is too low), 1.2% next year, which I think could be as much as 1% too low, and then I think an average of 1.1% for the next three years. My guess, because that’s what it is, albeit an educated one, is that growth will reach 1.5% this year, will be more than 2% next year, and will average about 2% over the following three years.

This is not some fantasy bullish dream; it would, in fact, be a growth rate a little below the economy’s long-term average. (2.1-2.3%)

To put that into context and using some rough and ready maths:

UK GDP in 2025: £3.04 trillion

Tax share of GDP will average about 38% over the period 2025 – 2030, according to the OBR.

My average growth rate forecast for the UK economy over the five-year period is roughly 2%.

NIESR’s average growth rate over the same period is roughly 1.2%.

Over five years, this produces a difference in nominal GDP (assuming we both use a 2% long-term inflation rate) of £140bn.

£140bn x 38% = £53.2bn

In other words, no black hole.

I suppose the bigger question here is why a Chancellor would be bullied into raising taxes by £50bn unnecessarily by a forecast that looks totally out of line with the UK’s long-term growth record. If she did so, it would inevitably undermine confidence in the economy and, by definition, lead to lower growth.

The answer, of course, is that she shouldn’t. Today’s tax policy should not be based on the gloom-laden forecasts of an institution that has not and should not earn the right to dictate the UK’s fiscal policy. (Its forecasting record is as bad as many other excessively gloomy institutions like the IMF and the OECD).

The Chancellor should adjust fiscal policy based on more contemporary, more certain, reliable data, just as the Bank of England appears now to be doing, having heeded Ben Bernanke's advice by reducing its dependence on much less reliable, longer-term forecasts when deciding what to do with interest rates.

I find it increasingly difficult to understand why the UK’s financial media is so relentlessly negative about the UK economy. Maybe it sells better than something more balanced. Perhaps it’s the product of lazy journalism or some self-loathing agenda. Either way, it risks creating its own reality and should be countered by a more realistic, grounded-in-facts narrative that the Chancellor might do well to start.

My advice would be to understand that we risk talking ourselves into a low-growth, sub-optimal outcome and take this threat seriously. It might be an opportunity to tell us that the government won’t be basing tax decisions today on long-term forecasts that change all the time, but on what’s actually happening in the economy right now.

Related reading

The UAE just walked out on OPEC. The real question is what Saudi Arabia does next.

The UAE's departure from OPEC isn't really about prices — it's about whether the cartel's whole operating model survives. The bigger question is what Saudi Arabia does next.

Read more

The retail data backs us up — the MPC should be cutting

The sharpest UK retail sales decline in over 40 years has just confirmed what Neil warned about on the podcast: the Bank of England's inflation fears were wrong, and the MPC should be cutting.

Read more

The Weapon That Wins Wars?

Why the blockade — not the bombs — is likely to end the Iran war, and why the IMF has mispriced the outcome.

Read moreStart investing with transparency

Access our full research, strategy insights, and real-time portfolio visibility.